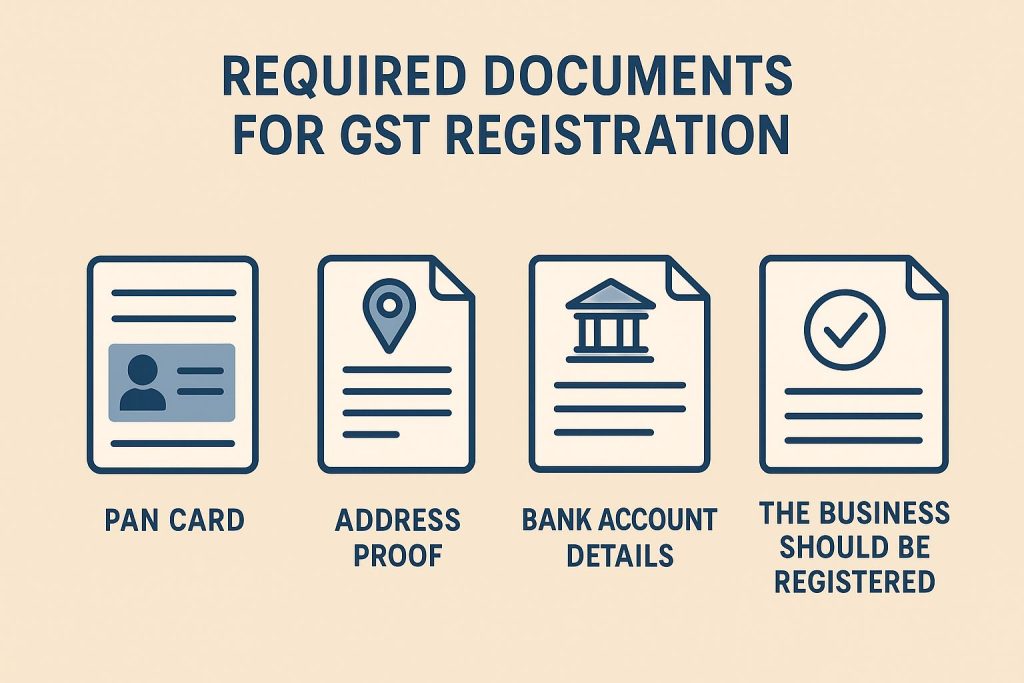

The documents required for Goods and Services Tax (GST) registration in India vary depending on the type of business entity (e.g., sole proprietorship, partnership, company). The core documents generally include a PAN card, proof of business address, identity and address proofs of key individuals, bank account details, and photographs.

Common Required Documents (for most business types)

1.Permanent Account Number (PAN) Card of the applicant/business entity.

2.Aadhaar Card of the proprietor, partners, or authorized signatories.

3.Photographs: Passport-size photos of the owner, partners, or directors (JPEG format, max 100 KB).

4.Business Address Proof:

Owned premises: Electricity bill, property tax receipt, municipal khata copy, or ownership deed.

Rented/Leased premises: Rent/lease agreement along with an ownership document (e.g., electricity bill) of the landlord. A No Objection Certificate (NOC) from the owner might also be needed.

5.Bank Account Details: A copy of a cancelled cheque or bank statement/passbook page showing the account number, name, and IFSC code (JPEG or PDF format).

6.Proof of Appointment of Authorized Signatory: A letter of authorization or a copy of a Board Resolution for companies/LLPs.

Entity-Specific Documents

1.Sole Proprietorship: No separate legal business documents are typically needed beyond the owner’s personal documents and business proofs.

2.Partnership Firm: Partnership deed.

3.Limited Liability Partnership (LLP):

4.LLP incorporation certificate.

5.LLP Agreement.

6.Digital Signature Certificate (DSC) is mandatory.

Private/Public Limited Company:

1.Certificate of Incorporation issued by the Ministry of Corporate Affairs (MCA).

2.Memorandum of Association (MOA) and Articles of Association (AOA).

3.Board Resolution appointing an authorized signatory.

4.PAN and address proof of all directors.

5.Digital Signature Certificate (DSC) is mandatory.

Tushar Tyagi

Rupesh Mangal & Associates

CHARTERED ACCOUNTANTS