If you’ve sold land, gold, shares, or any long-term capital asset other than a residential house, you may be staring at a large capital gains tax bill. But there’s a smart way to legally save tax — by investing in a residential property under Section 54F of the Income Tax Act, 1961.

In this guide, we’ll cover:

- Who is eligible

- Tax saving through reinvestment

- NRI-specific rules

- New ₹10 crore investment cap

- Tax rate and example calculations

🔍 What is Section 54F?

Section 54F offers exemption from long-term capital gains (LTCG) arising from the sale of assets other than a residential house, if the net sale consideration is reinvested in a residential house property in India.

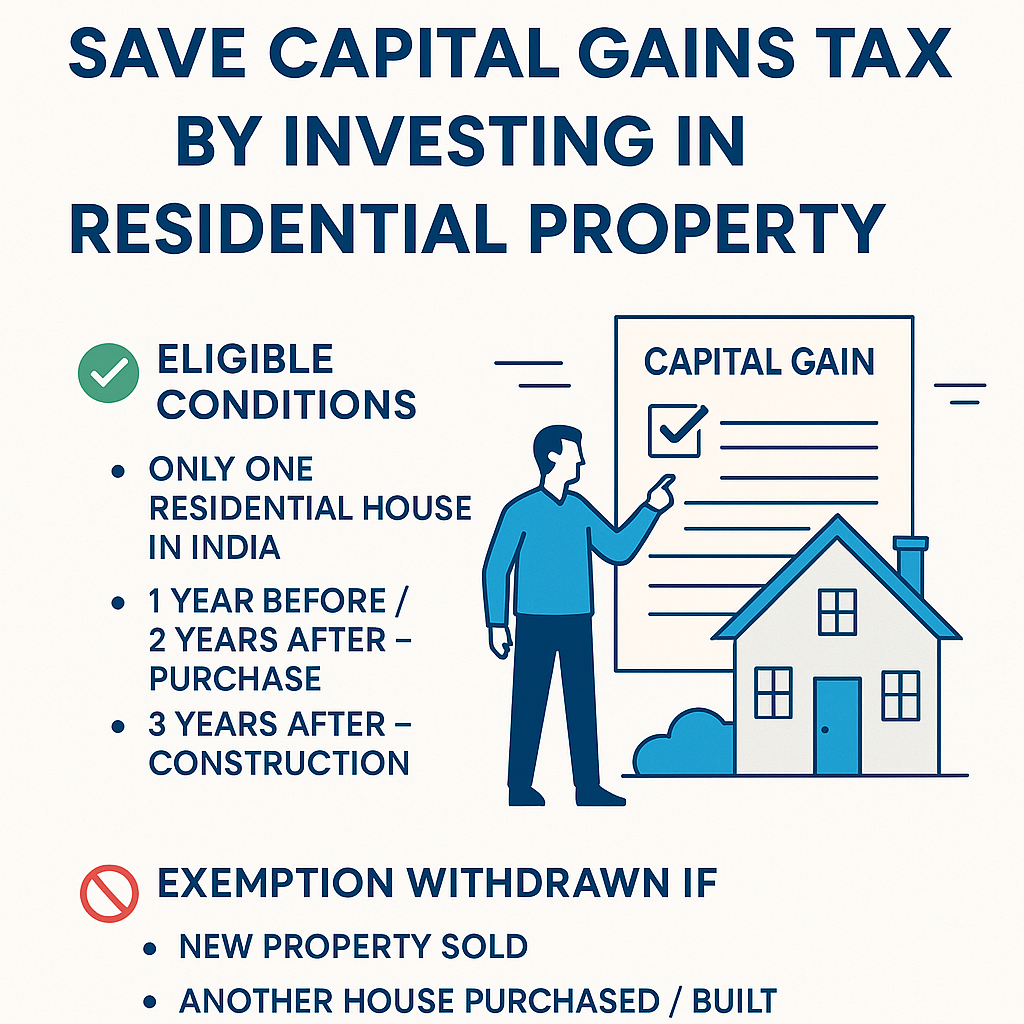

✅ Eligibility Criteria

Available to:

- Individuals

- HUFs

- Non-Resident Indians (NRIs)

Key conditions:

- The asset sold must be a long-term capital asset, not a residential house.

- You must not own more than one residential house (excluding the new one) on the date of transfer.

- The investment must be made in one residential house in India:

- Purchase within 1 year before or 2 years after the sale, or

- Construction within 3 years after the sale.

- The new house must not be sold within 3 years.

📈 How is the Exemption Calculated?

The exemption under Section 54F is proportional to the investment in the new house:

Exemption = LTCG × (Investment in new house / Net sale consideration)

🧮 Example:

- Net sale consideration = ₹80 lakh

- LTCG = ₹30 lakh

- Investment in new house = ₹60 lakh

➡️ Exemption = ₹30L × (60L/80L) = ₹22.5L

➡️ Taxable LTCG = ₹7.5L

🏦 Capital Gains Account Scheme (CGAS)

If you haven’t utilized the sale proceeds before the due date of ITR filing (usually 31st July), you must:

- Deposit the unutilized amount in a Capital Gains Account Scheme (CGAS).

- Use it within the allowed period for purchase/construction.

Failure to do so makes the exemption invalid, and LTCG becomes fully taxable.

🚨 NEW: ₹10 Crore Cap on Exemption

As per the Finance Act, 2023, a cap of ₹10 crore is now placed on exemption under Section 54 and Section 54F, effective AY 2024-25:

Even if you invest more than ₹10 crore in the new house, the maximum exemption is limited to ₹10 crore.

💡 Example with Cap Applied:

- Net sale consideration = ₹15 crore

- LTCG = ₹5 crore

- Investment = ₹12 crore

- Capped investment = ₹10 crore

➡️ Exemption = ₹5 Cr × (10 / 15) = ₹3.33 Cr

➡️ Taxable LTCG = ₹1.67 Cr

🌍 Section 54F for NRIs

Yes, NRIs can claim Section 54F, but must follow these:

| Condition | NRI Requirement |

|---|---|

| Asset Sold | Must be in India |

| Reinvestment | Only in residential property in India |

| Use of Funds | Preferably from repatriated funds |

| CGAS | Can be used if not invested before ITR filing |

🚫 When is Exemption Withdrawn?

The exemption is revoked and taxed if:

- The new residential house is sold within 3 years

- The taxpayer purchases or constructs another residential house within 2/3 years (other than the new one)

In such cases, the earlier exempted capital gain becomes fully taxable in the year of default.

🔚 Conclusion

Section 54F is a powerful tax-saving tool for residents and NRIs alike — especially when you’re planning to reinvest long-term capital gains into residential property. But post Budget 2023, the ₹10 crore cap means high-value investors need careful planning to avoid unexpected tax.

📞 Need Help?

Confused about capital gains tax or reinvestment strategy?