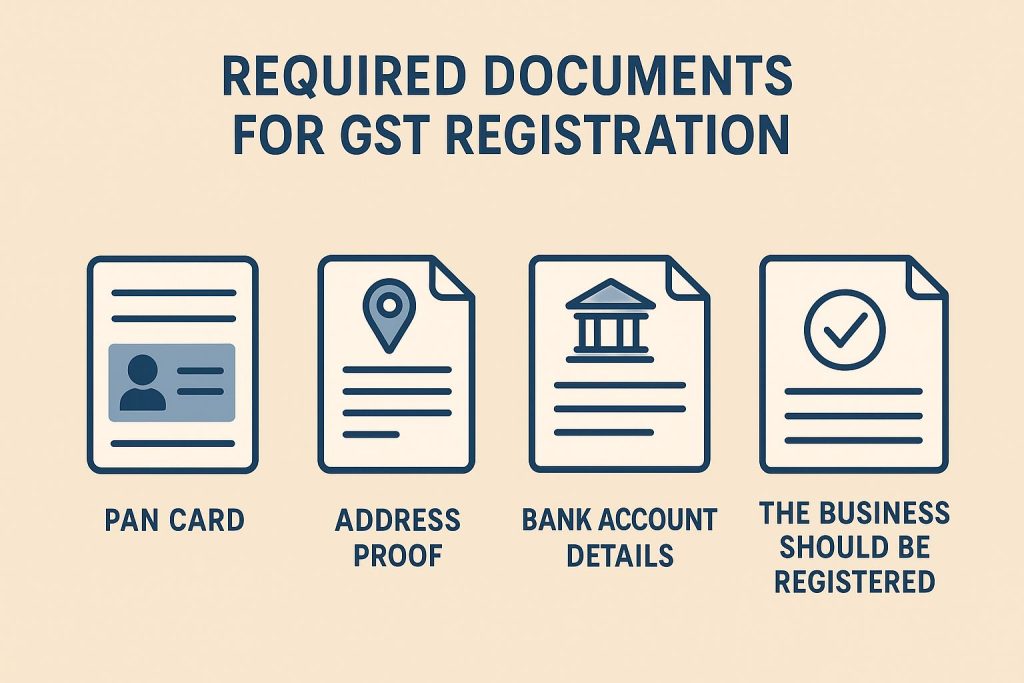

Common Required Documents (for most business types)

1.Permanent Account Number (PAN) Card of the applicant/business entity.

2.Aadhaar Card of the proprietor, partners, or authorized signatories.

3.Photographs: Passport-size photos of the owner, partners, or directors (JPEG format, max 100 KB).

4.Business Address Proof:

Owned premises: Electricity bill, property tax receipt, municipal khata copy, or ownership deed.

Rented/Leased premises: Rent/lease agreement along with an ownership document (e.g., electricity bill) of the landlord. A No Objection Certificate (NOC) from the owner might also be needed.

5.Bank Account Details: A copy of a cancelled cheque or bank statement/passbook page showing the account number, name, and IFSC code (JPEG or PDF format).

6.Proof of Appointment of Authorized Signatory: A letter of authorization or a copy of a Board Resolution for companies/LLPs.

Entity-Specific Documents

1.Sole Proprietorship: No separate legal business documents are typically needed beyond the owner’s personal documents and business proofs.

2.Partnership Firm: Partnership deed.

3.Limited Liability Partnership (LLP):

4.LLP incorporation certificate.

5.LLP Agreement.

6.Digital Signature Certificate (DSC) is mandatory.

Private/Public Limited Company:

1.Certificate of Incorporation issued by the Ministry of Corporate Affairs (MCA).

2.Memorandum of Association (MOA) and Articles of Association (AOA).

3.Board Resolution appointing an authorized signatory.

4.PAN and address proof of all directors.

5.Digital Signature Certificate (DSC) is mandatory.

Tushar Tyagi

Rupesh Mangal & Associates

CHARTERED ACCOUNTANTS

Proof of income and address: An ITR is a valid legal document that can be used as proof of both income and address for various financial and official purposes.

Easy loan approvals: Banks and financial institutions often require ITRs to assess your financial stability and repayment capacity when you apply for a home, car, or personal loan.

Claiming tax refunds: If you have paid excess tax through Tax Deducted at Source (TDS), you can claim a refund by filing an ITR.

Carry forward losses: You can carry forward capital losses or business losses to future years to offset them against future income, but only if you file your ITR on time.

Visa processing: Many countries require copies of your ITR to assess your financial stability during the visa application process.

Avoiding penalties: Timely filing helps you avoid penalties, interest on unpaid taxes, and other legal repercussions from the income tax department.

Higher insurance coverage: Insurance companies often ask for ITR records to determine your income, which can help you get higher coverage for term insurance plans.

Business opportunities: For entrepreneurs and startups, a filed ITR demonstrates financial transparency and may be required for obtaining government tenders or securing funding from investors.

Financial transparency: Filing an ITR promotes financial transparency by documenting your income and taxes, which fosters trust with financial institutions.

Tushar Tyagi,

Rupesh Mangal & Associates

CHARTERED ACCOUNTANTS

GSTR-1 & GSTR-3B (Normal Return) ₹50 per day (₹25 CGST + ₹25 SGST) and Maximum Late Fee annual turnover, up to 1.5 crore, then late fee 2000 (CGST + SGST) , annual turnover Between ₹1.5 Cr and ₹5 Crore then late fee 5000 (CGST + SGST), annual turnover Above ₹5 Crore, then late fee 10000 (CGST + SGST).

GSTR-1 & GSTR-3B (Nil Return) ₹20 per day (₹10 CGST + ₹10 SGST) and Maximum Late Fee ₹500 (₹250 CGST + ₹250 SGST)

GSTR-9 (Annual Return) ₹200 per day (₹100 CGST + ₹100 SGST) and Maximum Late Fee 0.5% of turnover in the State/UT (0.25% per Act)

GSTR-4 (Composition Scheme) ₹50 per day (₹20 for nil returns) and Maximum Late Fee ₹2,000 (₹500 for nil returns)

GSTR-10 (Final Return) ₹200 per day (₹100 CGST + ₹100 SGST) and Maximum Late Fee No upper limit specified

Interest on Late Payment of Tax

In addition to the late fee, interest is charged on the amount of tax that was not paid by the due date.

18% per annum on the outstanding tax liability, calculated daily from the day after the due date until the actual date of payment.

24% per annum for cases involving an undue or excess claim of Input Tax Credit (ITC) or an undue reduction in output tax liability.

Tushar Tyagi,

Rupesh Mangal & Associates

CHARTERED ACCOUNTANTS

Goods exempted under GST

Essential food items: Unbranded fresh fruits, vegetables, milk, eggs, honey, salt, and flour.

Agricultural products: Fresh ginger, turmeric, and seeds for planting.

Raw materials: Unprocessed raw silk, unspun jute fiber, and raw wool.

Books and publications: Printed books, newspapers, and journals.

Medical supplies: Human blood, plasma, and contraceptives.

Handloom and handicrafts: Certain items made by specially-abled persons and traditional artisans.

Services exempted under GST

Healthcare services: Provided by clinical establishments, authorized medical practitioners, and ambulance services.

Educational services: Provided by educational institutions to students, faculty, and staff, including transportation and mid-day meal services.

Agricultural services: Labor supply for farms, warehousing of agricultural produce, and renting of agricultural machinery.

Transportation services: Public transport by metro, bus (non-AC), or auto-rickshaws. Also includes transporting specific goods like milk and newspapers.

Charitable and religious services: Religious ceremonies and services by entities registered under Section 12AA.

Government services: Provided by the Central and State Governments and local authorities, with some exceptions.

Turnover-based GST exemption

For goods: The exemption limit for annual turnover is generally ₹40 lakhs. For special category states, the limit is ₹20 lakhs.

For services: The exemption limit for annual turnover is ₹20 lakhs in most states, and ₹10 lakhs in special category states.

Tushar Tyagi,

Rupesh Mangal & Associates

CHARTERED ACCOUNTANTS

]]>

The new regime has significantly fewer deductions available compared to the old regime.

The new tax regime offers lower tax rates but limits the available deductions and exemptions.

Standard Deduction: Salaried individuals and pensioners can claim a standard deduction of ₹75,000.

Family Pension: A deduction of ₹25,000 or one-third of the pension (whichever is less) is allowed from family pension income.

Employer’s Contribution to NPS: Deduction for the employer’s contribution to a National Pension System (NPS) account is allowed up to 14% of salary (for Central/State Government employees) or 10% (for others) under Section 80CCD(2). This is outside the common Section 80C limit.

Agniveer Corpus Fund: Contributions to the Agniveer Corpus Fund under Section 80CCH are allowed as a deduction.

Most common deductions like Section 80C, 80D, HRA exemption, and interest on self-occupied house property are not available under the new regime.

Tushar Tyagi,

Rupesh Mangal & Associates

CHARTERED ACCOUNTANTS

Filing Exemption Taxpayers with an aggregate annual turnover of up to ₹2 crore are exempt from filing GSTR-9.

GSTR-9C Mandate GSTR-9C (reconciliation statement) is mandatory for taxpayers with an aggregate turnover exceeding ₹5 crore.

ITC Reporting (Table 6) ITC claims are now segregated into current year credits and preceding year credits claimed in the current year using new Tables 6A1 and 6A2.

Reclaimed ITC A new Table 6H has been introduced to separately report ITC that was reversed in earlier periods (e.g., under Rule 37/37A) and subsequently reclaimed during FY 2024-25.

ITC Reversals (Table 7) Reversals must now be reported rule-wise (e.g., Rule 37, 37A, 42, 43, Section 17(5)), instead of in a consolidated manner.

Auto-Population (Table 8A) Table 8A, detailing available ITC, will auto-populate based on GSTR-2B and the document date, helping to align data with the actual financial year.

Prior Period Adjustments Tables 10, 11, 12, and 13 have undergone label changes and require more precise reporting of transactions and ITC adjustments related to FY 2024-25 but declared in subsequent returns (up to November 30, 2025).

HSN Details Reporting HSN codes in Table 17 (outward supplies) and Table 18 (inward supplies) remains mandatory, with specific digit requirements based on turnover.

Liability Payment Additional tax liability arising from reconciliation can now be settled via cash or ITC, a change from earlier rules that only allowed cash payments.

Tushar Tyagi,

Rupesh Mangal & Associates

CHARTERED ACCOUNTANTS

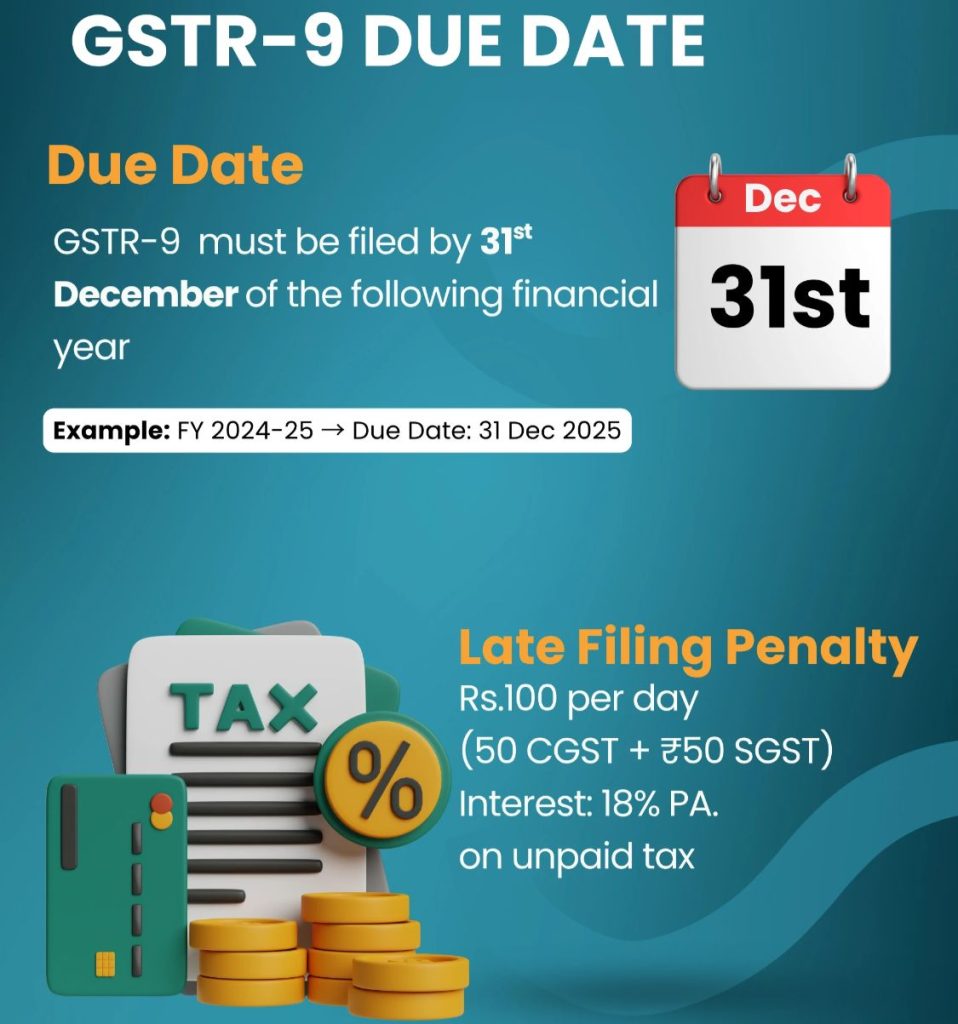

The due date for filing the GSTR-9 (Annual Return) for the financial year (FY) 2024-25 is December 31, 2025.

This date is typically the 31st of December of the year following the end of the financial year, unless officially extended by a notification from the government.

GSTR-9: This form is mandatory for all registered regular taxpayers with an annual aggregate turnover above a certain threshold (currently ₹2 crore for FY 2024-25).

GSTR-9C: Taxpayers with an annual turnover exceeding ₹5 crore are also required to file the GSTR-9C reconciliation statement, which is due on the same date as GSTR-9 (December 31, 2025).

]]>

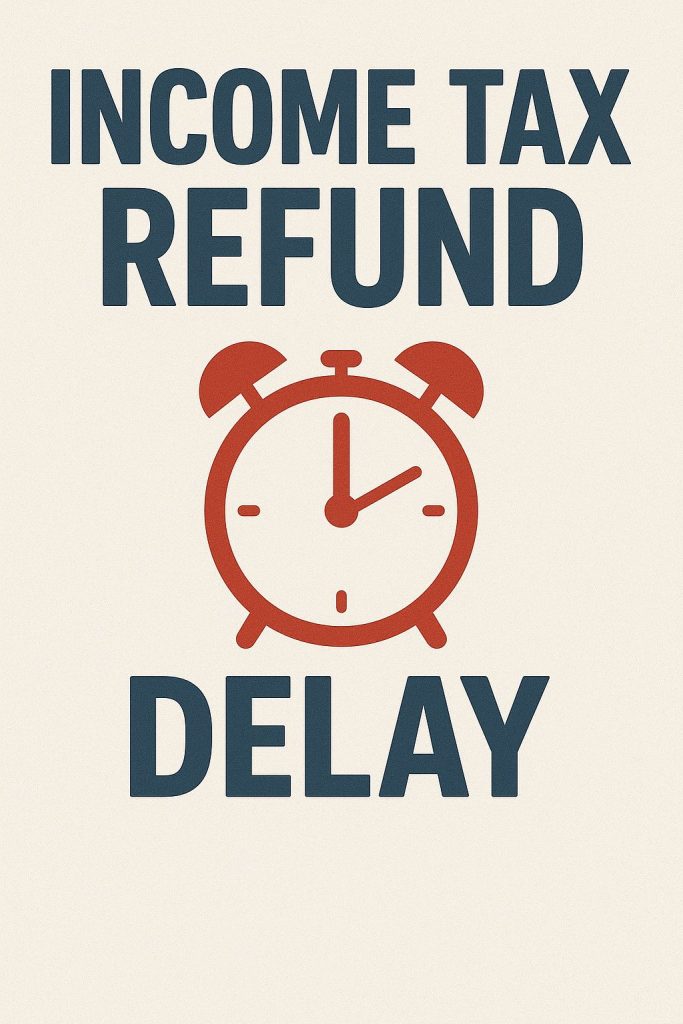

Common Reasons for AY 2025-26 Refund Delays

Increased Scrutiny: The IT department is conducting more detailed reviews and automated flagging of ITRs to ensure data accuracy and compliance, which slows down the overall processing time. Refunds in such cases are not processed until internal checks are complete.

Data Mismatches: Discrepancies between the information provided in your ITR and data available in Form 26AS, Annual Information Statement (AIS), or Taxpayer Information Summary (TIS) can trigger a delay and scrutiny.

Pending e-Verification: The ITR filing process is incomplete until the return is e-verified. No refund will be processed until this step is finalized.

Filing Close to the Due Date: Returns filed near the due date (September 16, 2025, for non-audit cases) experience delays due to the high volume of filings received by the department during that period.

Incorrect Bank Details: Errors in the provided bank account number or IFSC code can prevent the refund from being credited, even after processing.

]]>

Futures & Options (F&O) trading is treated as business income under the Income Tax Act. That means your reporting, tax calculation, and expense claims will follow business rules — not capital gains rules. Here’s a complete guide and a list of allowable trading expenses you can claim to reduce tax.

1. How to Calculate F&O Turnover (ICAI Method)

Turnover for F&O is not your total buy/sell value. It’s calculated as:

Turnover =

- Absolute profit/loss from each trade (ignore +/– sign)

- + Premium received on options sold

- + Differences in reverse trades (squared off)

Example:

| Trade Type | Buy Price | Sell Price | Qty | Profit/Loss | Turnover |

|---|---|---|---|---|---|

| NIFTY Future | 18,000 | 18,050 | 50 | ₹2,500 | ₹2,500 |

| BANKNIFTY Option Sell | ₹200 | ₹150 | 25 | ₹1,250 | ₹5,000 (premium) |

| BANKNIFTY Option Buy | ₹100 | ₹80 | 25 | -₹500 | ₹500 |

Total Turnover = ₹2,500 + ₹5,000 + ₹500 = ₹8,000

2. ITR Form & Reporting Format

- ITR Form: ITR-3

- Nature of Business Code: 21010 – Futures & Options Trading

A. Presumptive Taxation (Sec 44AD)

- Declare minimum 6% of turnover (if via banking) or 8% (cash — rare in F&O) as profit.

- No detailed P&L needed.

- Balance sheet: Only basic particulars (cash, bank balance, debtors, creditors, stock, fixed assets).

B. Normal Taxation (Actual Profits)

- Full P&L account with trading income and expenses.

- Full balance sheet showing assets & liabilities.

- Can claim all eligible business expenses.

3. Audit Requirements

Audit under Sec 44AB is mandatory if:

- Turnover > ₹10 crore, or

- Declaring profit < 6% of turnover under presumptive and total income > exemption limit, or

- Reporting a loss with total income > exemption limit.

4. Claimable F&O Trading Expenses

If you opt for normal taxation (not presumptive), you can deduct all expenses that are wholly and exclusively for trading, such as:

| Expense Type | Examples |

|---|---|

| Brokerage & Transaction Charges | Brokerage, STT (allowed for business), exchange fees |

| Internet & Communication | Broadband, mobile, trading platform subscriptions |

| Office Rent & Maintenance | Rent, cleaning, repairs |

| Electricity | Office or home office usage (proportionate) |

| Staff Salary | Office assistants, analysts, admin staff |

| Professional Fees | CA fees, tax consultant, research services |

| Software / Data Feeds | TradingView, Amibroker, broker APIs |

| Travel for Business | Broker visits, market seminars |

| Depreciation | Computers, office furniture, equipment |

Note:

- Keep bills and payment proofs.

- Claim proportionate amounts if partly personal (e.g., home electricity).

- Under presumptive taxation, you cannot claim these separately — expenses are assumed to be included in the declared profit.

5. Pro Tip for Investors + Traders

If you have both investment income (like long-term shares) and trading income (F&O), maintain two separate portfolios:

- Capital gains in Schedule CG

- Trading business income in Schedule BP

Bottom Line:

Bottom Line:

Report F&O income as business income in ITR-3, calculate turnover as per ICAI rules, choose between presumptive and normal taxation, and claim all legitimate expenses if using the normal method. Proper reporting not only reduces your tax liability but also keeps you safe from notices.

Talk to an expert now

Talk to an expert now